Well, compound interest is something like that, but on steroids! In fact, Albert Einstein is rumored to have said that "compound interest is the most powerful force in the Universe".

Given Einstein's love for the Universe and all its powerful forces, it does sound like he wanted us to take notice.

But what is it about compound interest that makes it so potent? Can a simple mathematical concept really have so much power over how we borrow and save so as to affect our financial well being?

Compound Interest - it's what makes us rich and it's what makes us poor

Most people are aware of the financial trouble that Greece found itself in back in 2007-2008. We also keep hearing about the United States hovering close to its "debt ceiling" every now and then. These are cases of debt ballooning over the years and reaching a level that could threaten to bring even rich and powerful nation states to a grinding halt. Debt in itself is scary enough, but when you add compounding interest to it, it can become crippling.

But, it's not all gloom and doom. There is a flip side to it. What if instead of paying this ever growing pile of money to someone, you were instead earning it? This is the promise behind many saving options like retirement plans, interest bearing saving accounts and even some stock market linked investments. Before we get into that though, let's look at what compounding interest really is.

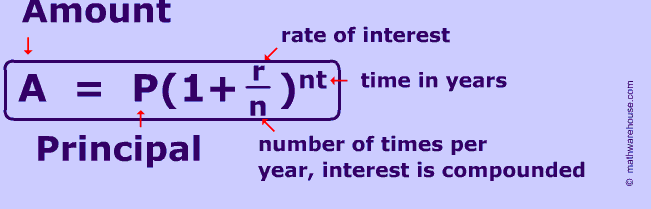

This formula can help you calculate the final amount with a compounded interest for any situation under the sun. Let's break it down into its components or "variables" as they are usually called.

A = This is the final amount at the end of the term of the loan/investment. It includes the principal as well as the compound interest accrued over time.

P = This is original principal amount at the beginning of the loan or investment.

r = This is the annual rate of interest. Keep in mind that 24% means 0.24 and 12% means 0.12 and so on.

t = This is the total time or duration of the loan in years. If the period is less than one year, you can use fractions. For example, 6 months would be 0.5 years and you can enter 0.5 in the formula.

n = This is the number of times the interest is compounded in a year. So in case of monthly compounding it would be 12; in the case of daily compounding it would be 365 and so on.

Most people (include seasoned investors) do not use this formula every time though. They simply use a calculator or some software like MS Excel and you can do the same here.

If you don't like looking at formulas, here is how it really works.

Let's assume we have a loan of $$ \$10,000$$ with $$ 24 \%$$ annual interest (which equals $$ 2\%$$ monthly) which is compounded every month.

This loan is equivalent to taking a loan for ONE month and then rolling it over 11 more times.

Let's start with the month of January.

Interest for January = $$2\%$$ of $$ \$10,000$$ = $$ \$200$$.

Now, we simply ADD this interest to the original principal to get the principal for February. So our new principal amount for February includes the original principal + the interest for January = USD 10,200.

Interest for February = 2% of USD 10,200 or USD 204.

And the principal for March equals = USD 10,200 + USD 204 = USD 10,404.

We can keep doing this for the each month and get the SAME result as with using the formula.

Annual Interest Rate

24%

Monthly Interest Rate

2%

Month

Principal Amount

Interest

January

10,000

200

February

10,200

204

March

10,404

208

April

10,612

212

May

10,824

216

June

11,041

221

July

11,262

225

August

11,487

230

September

11,717

234

October

11,951

239

November

12,190

244

December

12,434

249

A simple loan with monthly compounding

The total amount at the end of December is principal (USD 12,434 ) + interest (USD 249) = USD 12,682.

The math is good and all but how does it work in real life? Let's say that our friend Sally has a loan of USD 10,000. Let's say that her bank charges her an Annual Percentage Rate (APR) of 24%. Here are the different Examples:

Example 1: Simple Interest Rate (no compounding)

In this situation, Sally is simply charged an annual interest rate of 24% or USD 2,400 every year on her loan. Her total liability at the end is USD 12,400.

Example 2: Compound Interest – compounded monthly

Sally's annual rate is 24%, which gives us a monthly rate of 2%. We have already calculated this Example in the earlier table and we know the result is USD 12,682. Notice how this amount with compound interest is higher as compared to the amount in the simple interest Example.

Example 3: Compound Interest – compounded daily

But wait – it can get even more intense! If instead of monthly compounding, the bank does daily compounding (which is what many credit card companies actually do!), Sally's loan would balloon even faster. With the same annual rate of 24% with daily compounding, the original USD 10,000 becomes USD 12,711 by year end.

Here is what we get from our three Examples:

Simple Interest Rate (no compounding)

Compound Interest – compounded monthly

Compound Interest – compounded daily

Total Amount payable by December

USD 12,400

USD 12,682

USD 12,711

So there you have it. Even though the principal (USD 10,000) and the interest rate (24%) charged is the same, the frequency of compounding itself can have a significant difference in the total loan amount. The difference might not seem like much – but we have done the calculation for only one year and for a modest loan of USD 10,000. Over the course of your lifetime, the difference can easily be in the hundreds of thousands of dollars. It is certainly not something that you should be willing to ignore.

Fortunately, the immense multiplicative power of compound interest can work in our favor as well. A very basic example would be a simple saving account. If you put some money into it and forget about it - it will keep growing over time, just like the interest payments in our previous loan examples. However, the interest rate for savings accounts is not high enough for it to be an attractive option for saving.

This is where the various investment options come in. Whenever you reinvest money that you make from an investment, you are in a way gaining the benefit of compounding interest. In some cases you have to do it manually, but many investment plans do this for you automatically.

Let's take a look at a simple retirement plan which has a 7% annual rate of return, compounded annually. For simplicity's sake, we assume that the investment happened only once, rather than a recurring investment.

Sally invested USD 10,000 in this plan in 1990. Her friend Margaret invested USD 20,000 in the same plan in the year 2005. Let's see what their portfolios are worth now - at the end of 2017.

Using the calculator, we can see that Sally's investment is now worth USD 62,139.

Use the following values for the calculator:

P = USD 10,000

r = 0.07 (7%)

t = 27 years (from 1990 to 2017)

N = 1 (annual compounding)

Now let's look at how much money Margaret made, who invested twice the amount Sally did, but did so in 2005. Plugging the numbers into the calculator, we get USD 45,044.

This is the power of compounding. If you take a 401(k) account which not only gives you the benefit of compounding interest, but also tax savings and an incentive to invest annually - you can make a significant amount of saving. In fact, one of the main reasons the Government provides these tax benefits is so that citizens are further incentivized to take advantage of these saving plans and secure their futures financially.

Continuous compounding

As we have seen before, a daily compounding loan grows faster than a monthly compounding loan. Similarly, if you make the compounding hourly, the loan will grow even faster. Eventually, we reach a stage where the compounding period is so small that we consider it to be a continuously compounded loan.

It's practically impossible to calculate this by hand, but the power of mathematics gives us a formula to calculate the same. You can use the calculator at this link if you are interested.

However, you should not be worried about this too much as the impact of this continuous compounding is small. Also, very few loans are actually continuously compounded. As already mentioned, credit card are mostly compounded on a daily basis only.

Protecting your "interests"!

We have seen the power of compounding - both to drag the careless few further into debt, and to provide those who make a habit of saving with a comfortable and ever growing retirement cushion.

Before taking on any kind of loan (including credit cards!), make sure you are fully aware of what the exact terms of the loan are. Ask about the interest rates, ALL fees and charges and the compounding frequency. You can then plug these values into a calculator and get the exact amount that you would owe. The most important thing to remember for your financial well being is that even a small difference in charges, fees or interest rates can make a massive difference over time - especially with compound interest.